MP Board Class 12th Accountancy Important Questions Chapter 5 Dissolution of a Partnership Firm

Dissolution of a Partnership Firm Important Questions

Dissolution of a Partnership Firm Objective Type Questions

Question 1.

Choose the correct answer:

Question 1.

Profit on Realization is credited to Partner’s:

(a) Bank AJc

(b) Capital A/c

(c) Revaluation A/c

(d) Realization A/c.

Answer:

(b) Capital A/c

Question 2.

Assets and liabilities accounts are closed by transferring them into:

(a) Revaluation A/c

(b) Realization A/c

(c) Cash A/c

(d) Capital A/c.

Answer:

Question 3.

Compulsory dissolution of a firm:

(a) On the death of a partner

(b) On insolvency of a partner.

(c) On becoming insane of a partner

(d) When the business of the firm become illegal.

Answer:

(b) On insolvency of a partner.

Question 4.

Assets are transferred to Realization account on their :

(a) Book value

(b) Cost price

(c) Market price

(d) Establishment cost.

Answer:

(d) Establishment cost.

Question 5.

On payment of Liabilities, amount written :

(a) Book value

(b) Originally paid amount

(c) After deducting discount

(d) Any other price.

Answer:

(a) Book value

![]()

Question 6.

After transferring creditors and Bills payable to Realization account, if nothing is mentioned about its payment then these liabilities are:

(a) Not paid

(b) Fully paid

(c) Partially paid

(d) None of these.

Answer:

(b) Fully paid

Question 7.

When a partner pay the dissolution expenses on behalf of the firm, then these expenses will be debited in :

(a) Realization A/c

(b) Partner’s Capital A/c

(c) Partner’s loan A/c

(d) None of these.

Answer:

(a) Realization A/c

Question 8.

When unrecorded assets is taken over by a partner, it is shown in :

(a) Debit side of Realization A/c

(b) Debit side of Bank A/c

(c) Credit side of Realization A/c

(d) Credit side of Bank A/c.

Answer:

(c) Credit side of Realization A/c

Question 9.

When unrecorded liabilities are paid, it is shown in :

(a) Debit side of Realization A/c

(b) Debit side of Bank A/c

(c) Credit side of Realization A/c

(d) Credit side of Bank A/c.

Answer:

(a) Debit side of Realization A/c

Question 10.

Which of the following is an internal liability .

(a) Bank loan

(b) Bank overdraft

(c) General Reserve

(d) None of these.

Answer:

(c) General Reserve

![]()

Question 11.

On dissolution of firm all assets and liabilities are transferred to :

(a) Capital A/c

(b) Revaluation A/c

(c) Realization A/c

(d) None of these.

Answer:

(c) Realization A/c

Question 12.

The asset which is not transferred in realization A/c but it is sold :

(a) Stock

(b) Goodwill

(c) Investment

(d) None of these.

Answer:

(d) None of these.

Question 13.

Realization A/c is prepared :

(a) On admission of new partner

(b) On retirement of partner

(c) On dissolution of firm

(d) None of these.

Answer:

(c) On dissolution of firm

Question 14.

Dissolution of a firm, partner’s loan account is transferred to: (MP 2009 Set A)

(a) Realization account

(b) Partner’s capital account

(c) Partner’s current account

(d) None of these.

Answer:

(d) None of these.

![]()

Question 15.

Insolvency of a partner leads to which type of dissolution :

(a) Dissolution of agreement

(b) Compulsory dissolution

(c) Dissolution by incidence

(d) Dissolution by court.

Answer:

(b) Compulsory dissolution

Question 16.

Realization A/c is: (MP 2015,16)

(a) Real A/c

(b) Personal A/c

(c) Nominal A/c

(d) None of these.

Answer:

(c) Nominal A/c

Question 17.

At the time of dissolution of a firm Bank Overdraft is transferred to: (MP 2014)

(a) Cash A/c

(b) Realization A/c

(c) Capital A/c

(d) Revaluation A/c.

Answer:

(b) Realization A/c

Question 18.

Undistributed losses and reserves are transferred to: (MP 2017)

(a) Cash account

(b) Bank account

(c) Capital account of partners

(d) Profit & loss A/c.

Answer:

(c) Capital account of partners

![]()

Question 2.

Fill in the blanks:

- On the dissolution of firm the court appoint an ………………

- All the assets except ……………. are transferred to debit side of Realization account.

- Payment of liabilities is entered in …………….. side of cash account.

- The realized amount of assets is entered in ………….. account.

- All the Assets (except cash in hand and Bank) are transferred to ………….. side of …………. Account.

- All ……………… (External / Internal) liabilities are transferred to …………… side of …………… Account.

- Reserve loss / Undistributed losses are transferred to ……………… in their …………… ratio.

- When a partner took over any liability of the firm, his capital account is ………………

- Partner’s loan account is …………… in Realization Account.

- When a partner took over any assets of the firm, his capital account will be …………..

- Balance of Partner’s current account is transferred to partner’s …………… account.

- When all the partners of firm become insolvent except one then there is …………… dissolution of firm.

- Amount due to deceased partner is transferred to …………… account.

- By dissolution of partnership there is not compulsory dissolution of ……………..

- On dissolution of firm first of all ……………. liabilities are paid. (MP 2010)

- On dissolution of firm cash in hand is transferred to ………….. account.

- Realization account is a kind of …………….. account. (MP 2011)

- After dissolution of the firm, partner can transact their own ……………. (MP 2017)

Answer:

- Solicitor

- Cash & Bank balance

- Credit

- Realization

- Credit, Realization

- External, Debit, Realization

- Capital A/c, Profit Sharing ratio

- Debited

- Credited

- Not recorded

- Capital

- Compulsory

- legal executors

- firm

- outsiders

- cash

- real

- business.

![]()

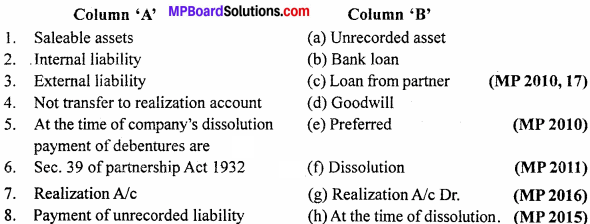

Match the columns:

Answer:

- (d) Goodwill

- (c) Loan from partner (MP 2010,17)

- (b) Bank loan

- (a) Unrecorded asset

- (e) Preferred (MP 2010)

- (f) Dissolution

- (h) At the time of dissolution. (MP 20I5)

- (g) Realization A/c Dr. (MP 2016)

Question 4.

Write true or false:

- Unrecorded assets are transferred to realization A/c.

- In a firm the dissolution of partnership among all partners is called dissolution of firm.

- Provision for bad debts is not transferred to realization A/c.

- Profit and loss of Realization A/c is divided among partners in profit and loss sharing ratio.

- Revaluation account is opened for closing the books of a firm under dissolution. (MP 2009 Set A)

- Balance sheet is prepared at the time of firm’s dissolution. (MP 2010,15)

- Partners loan is an internal liability. (MP 2010)

- The balance of realization account is transferred among partners in capital ratio.

- There are five methods of dissolution of firm. (MP 2011)

- The business is closed in case of dissolution of a firm. (MP 2012)

- Realization account is made many times in the life of a firm. (MP 2012)

- There is no difference between the dissolution of firm and dissolution of partner-ship. (MP 2016)

- On dissolution, payment made to creditors is debited to realization account. (MP 2017)

Answer:

- False

- False

- False

- True

- False

- False

- True

- False

- True

- True

- False

- False

- True.

![]()

Question 5.

Write the answer in one word / sentence:

- Realization account is prepared. (MP 2008,17)

- Assets and liabilities are transferred at book value. (MP 2012)

- The balance of current account is transferred.

- When liabilities of the partner are more than his assets, then he is called as ?

- The act which is applicable on dissolution of a firm.

- When all the partners or all the partners except one is declared insolvent then which type of dissolution it is ?

- At which value the assets of a dissolved firm are transferred to realization A/c.

- On the expiry of time the dissolution of partnership is called ? (MP 2016)

- On dissolution of firm, assets bought by partners is entered in Capital A/c in which side ?

- Profit or loss on Realization is divided among partners in which ratio ?

- Which assets are not transferred to Realization account ?

- Assets are transferred to Realization account in which value ?

- After the expiry of term, partnership that comes to an end is known ?

Answer:

- On dissolution of firm

- In realization account

- In capital account

- Insolvent

- Indian partnership act 1932

- Compulsory dissolution

- Book value

- Dissolution by co-incidence

- Debit side

- Profit sharing

- Cash & Bank balance

- Book value

- Partnership at will.

![]()

Dissolution of a Partnership Firm Very Short Answer Type Questions

Question 1.

What do you mean by dissolution of a partnership ?

Answer:

Dissolution of partnership firm means closing down the business of the firm. There is distinction between dissolution of partnership and dissolution of firm. Dissolution of partnership involves a change in the relation of partners, but the business is carried on. Section 39 of Indian Partnership Act, 1932 provides that, “The dissolution of partnership among all the partners of a firm is called the dissolution of the firm.”

Question 2.

What do you mean by realization account ?

Answer:

When the firm is dissolved, it is essential to close the accounts of various assets and liabilities. In this circumstance the assets are sold off and cash is realized. This cash is used for paying the liabilities. This process is entered in a separate account, which is known as realization account. It is a temporary account.

Question 3.

Write the names of those accounts entered in assets side of balance sheet which are not transferred to realization account.

Answer:

The following accounts are not transferred to realization account:

- Cash Account

- Bank Account

- Prepaid Expenses Account

- Accrued Income A/c

- Debit Balance of Profit and Loss Account.

Question 4.

Write the names of those accounts entered in the liability side of balance sheet which are not transferred to realization account.

Answer:

The following accounts are not transferred to realization account:

- Undivided Profit

- General Reserve

- Capital Account

- Partners Loan Account.

![]()

Question 5.

What journal entries are passed on sale of unrecorded Asset ?

Answer:

Cash A/c – Dr.

To Realization A/c

Question 6.

Which accounts are opened when a firm is dissolved ?

Answer:

The following accounts are opened when a firm is dissolved:

- Realization Account

- Partner’s Loan Account

- Partner’s Capital Account

- Cash Account or Bank Account.

Question 7.

In which condition partnership act will be dissolved ?

Answer:

According to Indian partnership Act section 43. When partnership act will be there then the firm can be dissolve by giving information to all the partners.

Question 8.

What do you mean by Compulsory dissolution of a firm ? Explain.

Answer:

Compulsory Dissolution: As per Indian partnership Act the compulsory dissolution of a firm takes place under the following conditions:

- When all the partners or all the partners except one partners are declared insolvent.

- When the business of the firm is declared illegal due to happening of any specific event.

- When the maximum number of members exceeds the stipulated Limit.

- When the citizen of an enemy nation is the partner of the firm.

![]()

Question 9.

Under what circumstances a court may order for the dissolution of a firm ? Explain.

Answer:

Court may order the dissolution of a firm if a partner files a suit for the purpose. The grounds on which such dissolution may be ordered are as under :

- When a partner became insane.

- When any of the firm’s partner becomes handicapped or permanently disabled.

- When any of the firm’s partner willfully breaches the agreement.

- When there is possibility of losses regularly in the firm’s business.

- On any other reason for which the court is satisfied that it is necessary to dissolve the firm.

Question 10.

Write the internal Liabilities which are not paid in cash by the firm during dissolution.

Answer:

Following are the internal Liabilities of any firm which are not paid in cash during firm’s dissolution.

Partner’s Capital A/c

Partner’s Loan A/c

Loan A/c of partner’s wife.

Question 11.

Which assets are not transferred in the debit side of Realization account but the amount received on their sale are entered in it ?

Answer:

Unrecorded assets are not transferred in the debit side of the Realization ac-count but the amount received on their sale are entered in it.

Question 12.

How do the left over or unrecorded assets and liabilities were recorded in realization A/c ? Explain .

Answer:

Unrecorded Assets and Liabilities are not transferred to realization account. But the amount received from the sale of unrecorded assets is entered in the credit side and payment made for unrecorded liabilities are entered in the debit side of realization account.

![]()

Question 13.

Which assets shown in the assets side of the balance sheet were not transferred to the realization account ?

Answer:

Cash in hand

Bank A/c

Dr. Balance of P/L A/c.

Question 14.

Which Liabilities shown in the liabilities side of the balance sheet were not transferred to the realization A/c ?

Answer:

Following liabilities were not transferred to the realization A/c :

- Undistributed profits

- General Reserve

- Partner’s Capital A/c

- Partner’s Loan A/c.

Question 15.

What is Memorandum balance Sheet ?

Answer:

Sometimes the partner’s capital accounts and all other liabilities were given in the question but the amount of total assets is not given. Under such condition, the amount of total assets is ascertained. Total of all the Liabilities is done on the basis of old balance sheet and from it, the amount of total sundry assets is calculated. Such a balance sheet is known as Memorandum Balance sheet.

![]()

Dissolution of a Partnership Firm Short Answer Type Questions

Question 1.

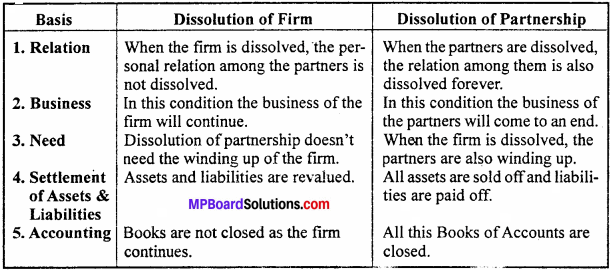

Write three differences between the dissolution of a firm and dissolution of part-pep?

Answer:

Differences between dissolution of a firm and dissolution of partners:

Question 2.

State the rules given under Section 48 of Partnership Act of 1932 to close the accounts when a firm is dissolved.

Or

How are accounts settled on dissolution of a firm ?

Answer:

The following rules are given under Section 48 of the Partnership Act of 1932 to close the accounts when a firm is dissolved:

(1) All the loss including the capital deficiency of the partners is adjusted at first from the profit, then from their capital balance and if need arise they have to bring in sufficient amount in their profit or loss sharing ratio.

(2) The realized amount from the sale of assets (including the amount brought by the partner) is used in the following order:

- The outside liabilities of the firm

- Proportionate payment of partner’s loan

- Payment of capital balance

- If any amount is left, it is shared by the partners in their profit or loss-sharing ratio.

![]()

Dissolution of a Partnership Firm Long Answer Type Questions

Question 1.

What accounts are opened on the dissolution of a firm ? Explain the realization account.

Answer:

When a partnership is dissolved, the following accounts are opened:

- Realization Account

- Partner’s Capital Account

- Bank/Cash Account

- Loan Account.

Realization account:

When a partnership is dissolved for closing all the assets and liabilities account and for entering the amount realized from the sale of assets and payments of all the liabilities, an account is opened, which is known as realization account. Preparation of realization account:

In the debit side of realization account, all the assets excluding cash and bank balance are entered. In the credit side of this account all the liabilities excluding the partners capital balance, partners loan towards the firm and the reserves are entered.

After that the amount received from the sale of assets credited and the payment of liabilities is debited in this account. After the dissolution, the balance of this account is transferred to all the partners capital account in their profit or loss sharing ratio.

Question 2.

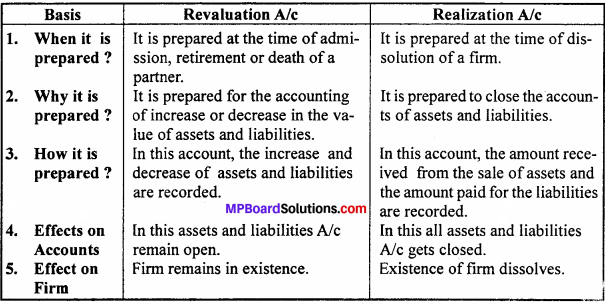

Differentiate between revaluation account and realization account.

Answer:

Differences between revaluation account and realization account:

![]()

Question 3.

which circumstances a partnership firm may be dissolved ?

Or

Explain the methods of dissolution of a firm.

Answer:

Section 40 to 44 of the Indian Partnership Act of 1932 tells that, on the following circumstances a partnership firm may be dissolved:

1. Dissolution by agreement:

A firm may be dissolved with the consent of all the partners or according to the terms of the agreement among the partners.

2. Compulsory dissolution:

Under section 41 of the Indian partnership act 1932, by the adjudication of all the partners but one as insolvent, or by the business of the firm becomes unlawful or illegal due to the happening of any such incident or event, the firm may be compulsory dissolved.

3. Dissolution by court: If any of the circumstances lays down, the court may under to dissolve the firm:

- When a partner becomes unsound mind

- When a partner suffers from permanent incapacity and incapable for performing his duties as a partner

- When a partner is found guilty out of misconduct affecting the firm

- On the will full and persistent breach of partnership agreement by a partner

- On the transfer of the whole or the interest by a partner in favor of a third party or when his share is attached

- under a decrease or sold under process of law.

- When the business of the firm can’t be carried on.

- On any other just and equitable ground.

4. Dissolution on the happening of contingencies: A firm may be dissolved in any of the following ways unless there is a contract between the partners to the contrary:

- By expiry of the term fixed

- By the completion of the adventure that which the firm is constituted

- By the death of a partner

- By the adjudication of a partner as insolvent.