MP Board Class 11th Accountancy Important Questions Chapter 9 Trial Balance

Trial Balance Important Questions

Trial Balance Objective Type Questions

Question 1.

Choose the correct answer:

Question 1.

What kind of accuracy is tested by Trial balance –

(a) Theoritical

(b) Practical

(c) Arithmetical

(d) None of these.

Answer:

(c) Arithmetical

Question 2.

How many methods are there for preparing Trial Balance –

(a) One

(b) Three

(c) Four

(d) None of these.

Answer:

(c) Four

![]()

Question 3.

Which of the following is prepared on the basis of Trial Balance –

(a) Journal

(b) Ledger

(c) Final Accounts

(d) None of these.

Answer:

(c) Final Accounts

Question 4.

Of the two sides of Trial balance does not tally, which Account is opened –

(a) Suspense Account

(b) Personal Account

(c) Real Account

(d) None of these.

Answer:

(a) Suspense Account

Question 5.

The error which can be disclosed by Trial balance –

(a) Error of ommission

(b) Error of principal

(c) Compensatory error

(d) None of these.

Answer:

(d) None of these.

Question 2.

Fill in the Blanks:

- Trial balance is merely a …………… not an Account.

- …………….. are prepared on the basis of Trial balance.

- Trial balance is a test of …………….. Accuracy.

- Generally …………… does not form a part of Trial balance.

- ……………. stock is not included in Trial balance.

Answer:

- Statement

- Final Accounts

- Arithmetical

- Closing stock

- Closing stock.

Question 3.

Answer in one word/sentence:

- “A Trial balance is a statement of debit and Credit Balances Extracted from the ledger with a view to test the arithmetical accuracy of the books.” Who said this?

- Mention any account which can show Debit or Credit Balance.

- Debtor’s Accounts always show which balance?

- What Balance is shown by Drawing Account?

- How many methods are there for preparing trial balance?

- Is trial balance Ultimately proof of accuracy of accounts?

- What is the nature of suspense A/c ?

Answer:

- J.R. Batliboi

- Rent

- Debit

- Debit

- Four methods

- No

- Fluctuating.

![]()

Question 4.

State True or False:

- Closing stock appears outside the trial balance.

- A trial balance is not a conclusive proof of accounting accuracy.

- Trial balance is a test of only Arithmetical accuary.

- Trial balance helps to check the principles of Double Entry System.

- Trial balance is a part of ledger.

Answer:

- True

- True

- True

- True

- False.

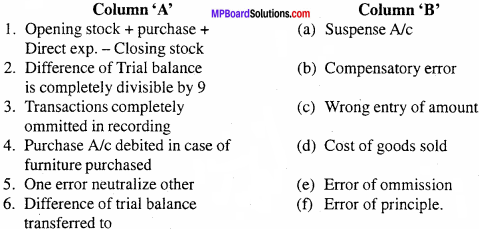

Question 5.

Match the following:

Answer:

1. (d)

2. (c)

3. (e)

4. (f)

5. (b)

6. (a).

Trial Balance Short Answer Type Questions

Question 1.

Define trial balance. Discuss its objects.

Answer:

A trial balance may be defined as “A trial “balance is not an account. It is a statement or a test of debit and credit balances of all ledger accounts as on a given date, prepared with the object of proving the arithmetical accuracy of ledger accounts”.

The main objects of preparing a trial balance are:

- The balance of any ledger account can be easily found from the trial balance without going through the pages of the ledger book.

- To check the arithmetical accuracy of the books.

- It is a base for the preparation of final accounts.

Question 2.

Mention the merits and demerits of balance method of preparing trial balance.

Answer:

Following are the merits and demerits of balance method:

- Helpful in preparing final accounts – With the help of balances from trial balance in this method, final accounts are prepared.

- Small size – Some accounts show no balance and hence they are not recorded in trial balance. Hence the size reduces.

- Less chance of error – Due to small size, the totalling becomes easy and the chances of errors are minimised.

![]()

Question 3.

Explain the preparation of trial balance under balancing method.

Answer:

Under this method, each account is totalled and balanced. Then this balance is transferred to the trial balance. If a particular account shows a debit balance, it is transferred to the debit balance column of trial balance and vice versa. At the end, both the columns are totalled in the trial balance. There should not be any difference. If there is some difference, there is some mistake and it must be corrected.

Question 4.

What is suspense account?

Answer:

Even after checking of journal and ledger completely, the errors are not located, then the difference amount is transferred to a temporary account, i.e., suspense account in order to tally the Trial Balance. In future, when errors are detected, suspense account is closed.

Trial Balance Long Answer Type Questions

Question 1.

Is trial balance a conclusive proof of accuracy of accounts? Explain.

Or

Explain the errors which are not disclosed by a trial balance.

Answer:

Generally, it is treated that, when the debit total and credit total agrees, the ledger accounts are prepared correctly. But then also it is not possible to agree with the accuracy of accounts because there are some errors which are not disclosed by a trial balance and the trial balance may agree. They are as follows:

1. Errors of omission:

If an entry is omitted to record in journal, it will not reflected in ledger accounts and trial balance, such type of an error, will not be disclosed by a trial balance. This type of an error is called ‘Errors of omission’ e.g., Sold goods to Mr. Kshitij for 5,000 is not entered in Journal.

2. Errors of principle:

When the transactions are entered against the principles of double entry system, it is said to be Errors of Principle’. For e.g. Machinery purchased for Rs. 5,000 is entered in purchase account. As per the rule of D.E.S. when an asset buys that particular asset is debited. This type of error will not be disclosed by the trial balance.

3. Compensating errors:

These are those errors where one error is compensated with another error, e.g., In wages A/c, it is entered Rs. 100 less and in salary account it entered Rs. 100 more. In this condition, both are errors. But one error is adjusted with another error. This type of error will not affect the agreement of trial balance and it will not be disclosed there.

4. Wrong posting in ledger accounts:

When journal entries are posted wrongly in ledger account, it will affect the agreement of trial balance, e.g., Instead of salary paid Rs. 1,000 entered in wages account with the same amount. This type of error will not disclose by the trial balance.